Life insurance is one of the most important financial tools for protecting your family’s future. It ensures that your loved ones are financially secure if something unexpected happens to you. However, many people believe that getting high coverage life insurance is expensive and out of reach. The truth is, with the right strategies, you can secure affordable life insurance with high coverage without overpaying.

In this comprehensive guide, you will learn how life insurance works, what affects pricing, and most importantly, how to get the best possible coverage at the lowest cost.

Understanding Life Insurance and Why Coverage Matters

Life insurance is a contract between you and an insurance provider. In exchange for regular payments (called premiums), the insurer promises to pay a lump sum (death benefit) to your beneficiaries when you pass away.

High coverage means a larger payout—often enough to cover:

- Mortgage or rent

- Children’s education

- Daily living expenses

- Outstanding debts

- Long-term family financial security

The challenge is balancing affordability and coverage size. Many people either underinsure themselves to save money or overpay for unnecessary features.

Types of Life Insurance You Should Know

Before choosing a policy, you must understand the two main types of life insurance:

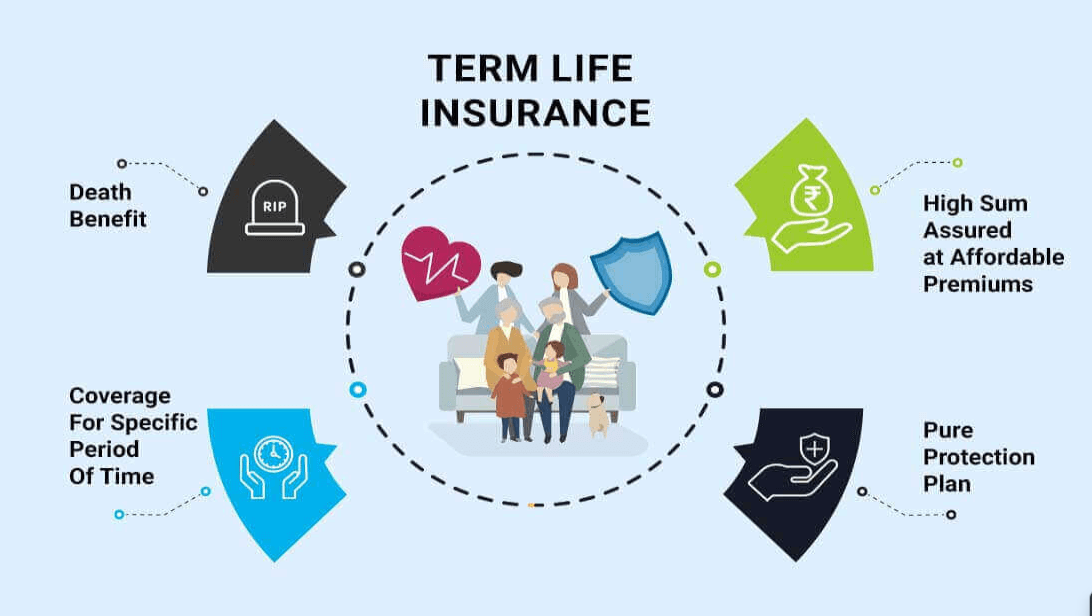

1. Term Life Insurance

Term life insurance provides coverage for a specific period (10, 20, or 30 years).

Advantages:

- Lower premiums

- High coverage at affordable cost

- Simple structure

Best for: Families, young professionals, and individuals with financial responsibilities

2. Whole Life Insurance

Whole life insurance provides lifelong coverage and includes a cash value component.

Advantages:

- Lifetime protection

- Builds cash value

- Fixed premiums

Disadvantages:

- Higher cost

- More complex structure

If your goal is affordable high coverage, term life insurance is usually the best option.

Factors That Affect Life Insurance Costs

Understanding what influences your premium helps you find ways to reduce costs.

1. Age

The younger you are, the cheaper your policy. Premiums increase significantly as you age.

2. Health Condition

Insurance companies assess your health through medical exams or questionnaires. Conditions like diabetes, hypertension, or obesity can increase costs.

3. Lifestyle Choices

Smoking, alcohol consumption, and risky hobbies (like extreme sports) raise premiums.

4. Coverage Amount

The higher the coverage, the more you pay. However, the cost per $1,000 of coverage often decreases with larger policies.

5. Policy Term

Longer terms typically cost more but provide extended protection.

How to Get Affordable Life Insurance with High Coverage

Now let’s explore practical strategies to maximize coverage while minimizing cost.

1. Buy Life Insurance Early

One of the most effective ways to get affordable premiums is to buy insurance as early as possible.

A 25-year-old will pay significantly less than a 40-year-old for the same coverage. Waiting too long increases risk factors such as health issues, which raise costs.

Key takeaway: The earlier you start, the cheaper your long-term protection becomes.

2. Choose Term Life Insurance for Maximum Value

If your goal is high coverage at low cost, term life insurance is the smartest choice.

For example:

- $500,000 coverage might cost only a small monthly premium for a healthy young adult

- Whole life insurance for the same coverage could cost 5–10 times more

Term insurance gives you maximum financial protection during your most important earning years.

3. Compare Multiple Insurance Providers

Never settle for the first quote you receive. Insurance pricing varies significantly between companies.

By comparing at least 5–10 providers, you can:

- Find lower premiums for the same coverage

- Discover better policy benefits

- Avoid hidden fees

Online comparison tools make this process fast and efficient.

4. Improve Your Health Before Applying

Insurance companies reward healthy individuals with lower rates.

Simple improvements include:

- Losing excess weight

- Quitting smoking

- Reducing alcohol intake

- Exercising regularly

- Improving cholesterol and blood pressure levels

Even small health improvements can lead to significant savings over time.

5. Avoid Unnecessary Policy Add-Ons

Insurance companies often offer riders such as:

- Critical illness coverage

- Accidental death benefit

- Waiver of premium

While some riders are useful, many are unnecessary if your goal is affordability.

Only choose add-ons that match your actual financial needs.

6. Choose the Right Coverage Amount

Many people overestimate how much coverage they need, leading to higher premiums.

A simple formula to estimate coverage:

- 10–15 times your annual income

- Plus outstanding debts

- Plus future education expenses for children

This ensures your family is protected without overpaying for excessive coverage.

7. Pay Annually Instead of Monthly

Insurance companies often charge extra fees for monthly payments.

Paying annually can:

- Reduce total cost

- Eliminate administrative charges

- Provide discounts in some cases

This is a simple but effective cost-saving strategy.

8. Maintain a Healthy Lifestyle Long-Term

Even after buying a policy, maintaining good health is important.

Some insurers offer:

- Renewal discounts

- Healthy lifestyle rewards

- Lower long-term premium increases

Healthy habits not only save money but also improve your quality of life.

9. Take Advantage of Employer-Provided Insurance

Many employers offer group life insurance at lower rates or even free coverage.

While this may not be enough on its own, it can:

- Supplement your personal policy

- Reduce the total coverage you need to purchase individually

10. Work With a Licensed Insurance Agent

A professional insurance agent can help you:

- Compare multiple policies

- Find hidden discounts

- Customize coverage based on your needs

However, ensure the agent is independent and not tied to a single company.

Common Mistakes to Avoid

Many people end up overpaying or underinsuring themselves due to common mistakes:

1. Waiting Too Long to Buy Insurance

Delaying your decision increases premiums significantly.

2. Choosing the Cheapest Policy Without Checking Coverage

Low cost is useless if coverage is insufficient.

3. Ignoring Policy Terms

Always read the fine print to avoid surprises.

4. Not Reviewing Coverage Regularly

Life changes such as marriage, children, or debt should trigger policy updates.

Real Example of Cost Optimization

Let’s compare two individuals:

Person A:

- Age: 25

- Healthy

- Buys $500,000 term life insurance

- Pays low monthly premium

Person B:

- Age: 40

- Some health issues

- Buys same $500,000 coverage

- Pays 2–3 times more

This clearly shows how timing and health directly impact affordability.

Why High Coverage Is Still Important

Some people reduce coverage to save money, but this can be dangerous.

High coverage ensures:

- Family financial stability

- Debt protection

- Education funding for children

- Long-term peace of mind

The goal is not just affordability, but balanced financial protection.

Final Thoughts

Getting affordable life insurance with high coverage is absolutely possible if you apply the right strategies. The key is to start early, choose the right type of policy, compare providers, and maintain a healthy lifestyle.

Instead of focusing only on price, focus on value and long-term protection. A well-structured life insurance policy is not just an expense—it is a financial safety net that protects everything you’ve worked hard to build.

By following the steps in this guide, you can secure strong coverage without straining your budget, ensuring peace of mind for you and your family for years to come.