Insurance is one of the most important financial tools in modern life. It helps protect individuals and families from unexpected financial losses that can occur due to accidents, illness, or death. Among the many types of insurance available today, life insurance and auto insurance are two of the most commonly purchased policies.

Although both serve the purpose of financial protection, they are fundamentally different in terms of coverage, purpose, structure, and benefits. Understanding these differences is essential for making informed financial decisions.

In this article, we will explore life insurance vs auto insurance, their key differences, how they work, and the benefits each provides.

What Is Life Insurance?

Life insurance is a financial contract between an individual and an insurance company. In this agreement, the policyholder pays regular premiums, and in return, the insurer provides a lump-sum payment (known as a death benefit) to designated beneficiaries after the policyholder’s death.

How Life Insurance Works

Life insurance is designed to provide financial protection for your loved ones in the event of your passing. The policyholder chooses:

- Coverage amount (death benefit)

- Beneficiaries

- Policy type (term or permanent)

- Premium payment schedule

If the insured person dies during the coverage period, the insurance company pays the agreed amount to the beneficiaries. Some policies may also include savings or investment components.

Types of Life Insurance

- Term Life Insurance

- Coverage for a specific period (10, 20, or 30 years)

- Lower premiums

- No payout if the term expires while the insured is alive

- Whole Life Insurance

- Lifetime coverage

- Includes cash value accumulation

- Higher premiums but long-term benefits

- Universal Life Insurance

- Flexible premiums and coverage

- Investment component

- Adjustable death benefits

What Is Auto Insurance?

Auto insurance is a policy that provides financial protection against losses related to vehicles. It covers damages caused by accidents, theft, natural disasters, or liability for injuries and property damage to others.

How Auto Insurance Works

When you purchase auto insurance, you agree to pay premiums in exchange for coverage that helps pay for:

- Vehicle repairs or replacement

- Medical expenses after an accident

- Legal liability if you cause damage or injury

- Theft or vandalism losses

Auto insurance is mandatory in many countries because it ensures that drivers can cover damages they may cause on the road.

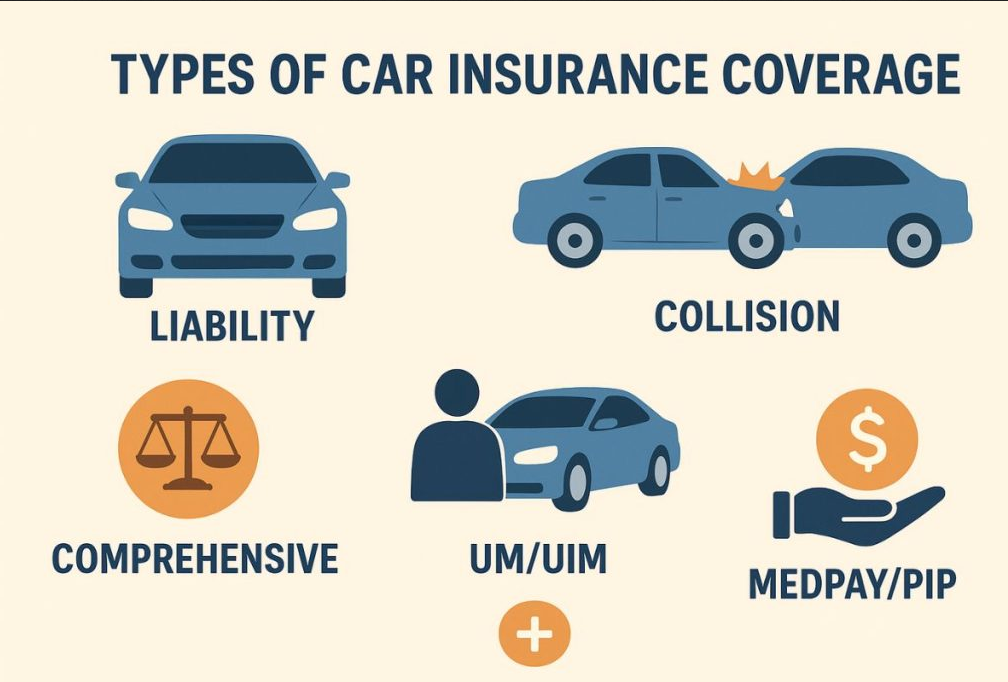

Types of Auto Insurance Coverage

- Liability Coverage

- Covers damage or injuries you cause to others

- Collision Coverage

- Pays for damage to your own vehicle after an accident

- Comprehensive Coverage

- Covers non-collision incidents like theft, fire, or natural disasters

- Personal Injury Protection (PIP)

- Covers medical expenses for you and passengers

Key Differences Between Life Insurance and Auto Insurance

Although both are forms of protection, life insurance and auto insurance differ in several important ways.

1. Purpose of Coverage

- Life Insurance: Provides financial security to family members after the policyholder’s death.

- Auto Insurance: Covers vehicle-related risks and liabilities while driving.

2. Policy Trigger Event

- Life Insurance: Activated upon death or, in some cases, terminal illness.

- Auto Insurance: Activated when accidents, theft, or vehicle damage occur.

3. Beneficiaries

- Life Insurance: Beneficiaries are family members or dependents.

- Auto Insurance: Policyholder or third parties affected by accidents.

4. Duration of Coverage

- Life Insurance: Can last for a fixed term or lifetime.

- Auto Insurance: Usually renewed annually or semi-annually.

5. Mandatory Requirement

- Life Insurance: Optional in most cases.

- Auto Insurance: Legally required in many regions.

6. Financial Benefit Structure

- Life Insurance: Pays a lump sum (death benefit).

- Auto Insurance: Pays for repairs, medical bills, or liability claims.

Benefits of Life Insurance

Life insurance is more than just a financial product—it is a long-term safety net for families.

1. Financial Protection for Loved Ones

The primary benefit is ensuring your family is financially secure even after your death. It helps cover:

- Daily living expenses

- Mortgage payments

- Education costs

- Debt repayment

2. Debt Coverage

Life insurance can help pay off outstanding debts such as loans, credit cards, or mortgages so your family is not burdened.

3. Income Replacement

If you are the primary earner, life insurance replaces your income to maintain your family’s lifestyle.

4. Wealth Transfer

Some policies allow you to pass wealth to future generations in a tax-efficient manner.

5. Cash Value Growth (Permanent Policies)

Whole life and universal life insurance policies accumulate cash value that can be borrowed or withdrawn.

Benefits of Auto Insurance

Auto insurance provides critical protection for drivers and vehicle owners.

1. Financial Protection Against Accidents

Accidents can be expensive. Auto insurance helps cover:

- Vehicle repairs

- Medical expenses

- Legal costs

2. Legal Compliance

In many countries, having auto insurance is required by law. It ensures drivers are financially responsible.

3. Protection Against Theft and Damage

Comprehensive coverage protects your vehicle from:

- Theft

- Vandalism

- Natural disasters

- Fire damage

4. Peace of Mind While Driving

Knowing you are financially protected reduces stress while driving.

5. Liability Protection

If you cause an accident, auto insurance covers damages to other people’s property or injuries.

Cost Comparison: Life Insurance vs Auto Insurance

Life Insurance Costs

Life insurance premiums depend on:

- Age

- Health condition

- Coverage amount

- Policy type

- Lifestyle habits (smoking, occupation)

Generally, younger and healthier individuals pay lower premiums.

Auto Insurance Costs

Auto insurance premiums depend on:

- Type of vehicle

- Driving history

- Location

- Coverage type

- Age and experience of driver

Drivers with clean records usually pay less.

Which Insurance Do You Need More?

The answer depends on your lifestyle and financial responsibilities.

You Need Life Insurance If:

- You have dependents (spouse, children, parents)

- You have outstanding debts

- You want to secure your family’s future

- You are the primary income provider

You Need Auto Insurance If:

- You own or drive a vehicle

- You want protection against accidents

- You want legal compliance

- You want financial protection from repair costs

Ideally, most people benefit from having both types of insurance simultaneously.

Real-Life Example Comparison

Scenario 1: Life Insurance

John, a 35-year-old father, has a wife and two children. If John passes away unexpectedly, his life insurance policy provides financial support to cover living expenses, education, and mortgage payments.

Scenario 2: Auto Insurance

Sarah, a 28-year-old driver, gets into a car accident. Her auto insurance covers the repair costs of her car and medical bills, preventing financial hardship.

Common Misconceptions

Misconception 1: Life Insurance Is Only for the Elderly

In reality, younger individuals benefit more because premiums are lower.

Misconception 2: Auto Insurance Only Covers Car Damage

It also includes medical costs, liability, and theft protection.

Misconception 3: Insurance Is a Waste of Money

Insurance is not an expense—it is financial protection against high-risk events.

How to Choose the Right Insurance

For Life Insurance

- Compare policy types

- Evaluate coverage needs

- Choose reputable insurers

- Consider long-term affordability

For Auto Insurance

- Compare coverage options

- Check deductibles

- Review claim process efficiency

- Look for discounts (safe driver, multi-policy)

Can You Have Both Life and Auto Insurance?

Yes—and most financially responsible individuals do. Having both ensures complete protection:

- Life insurance protects your family

- Auto insurance protects your vehicle and driving liability

Together, they form a strong financial safety system.

Conclusion

Life insurance and auto insurance serve different but equally important purposes. Life insurance focuses on long-term financial protection for your loved ones in the event of death, while auto insurance protects you from financial losses related to driving and vehicle ownership.

Understanding the differences between these two types of insurance helps you make smarter financial decisions and ensures that you are fully protected in all aspects of life.

Ultimately, the best approach is not choosing one over the other, but rather understanding how both work together to provide comprehensive financial security.